8 Insurance Claim Mistakes to Avoid After an Auto Accident - From an Adjuster

After a car accident, many drivers focus on the immediate steps: checking for injuries, documenting the scene, and reporting the crash.

But what happens after the claim is opened can also have a major impact on how smoothly the process goes.

Insurance claims involve investigations, documentation, and sometimes negotiations. Certain actions—or inactions—can unintentionally complicate that process.

Understanding a few common mistakes can help drivers avoid unnecessary delays and frustration.

Mistake #1: Waiting Too Long to Report the Accident

One of the most common issues adjusters encounter is delayed reporting.

Drivers sometimes wait days—or even weeks (I’ve even had someone wait years)—before notifying their insurance company.

This can create problems because:

Evidence disappears

Witness memories fade

Vehicle damage may change

Injuries become harder to connect to the accident

Most insurance policies require drivers to report accidents promptly.

Even if you’re unsure whether you plan to pursue a claim, it’s generally better to report the incident early and allow the insurance company to document what happened.

Mistake #2: Not Gathering Enough Evidence at the Scene

Another frequent mistake happens in the first few minutes after a crash.

Drivers may exchange information and leave the scene without taking photos or documenting important details.

Later, when the claim investigation begins, everyone is trying to remember what happened—but the evidence is gone.

Photos of:

Vehicle damage

The surrounding area

Traffic signals

Road conditions

can become extremely valuable during a liability investigation.

Without documentation, many claims become one driver’s word against another’s.

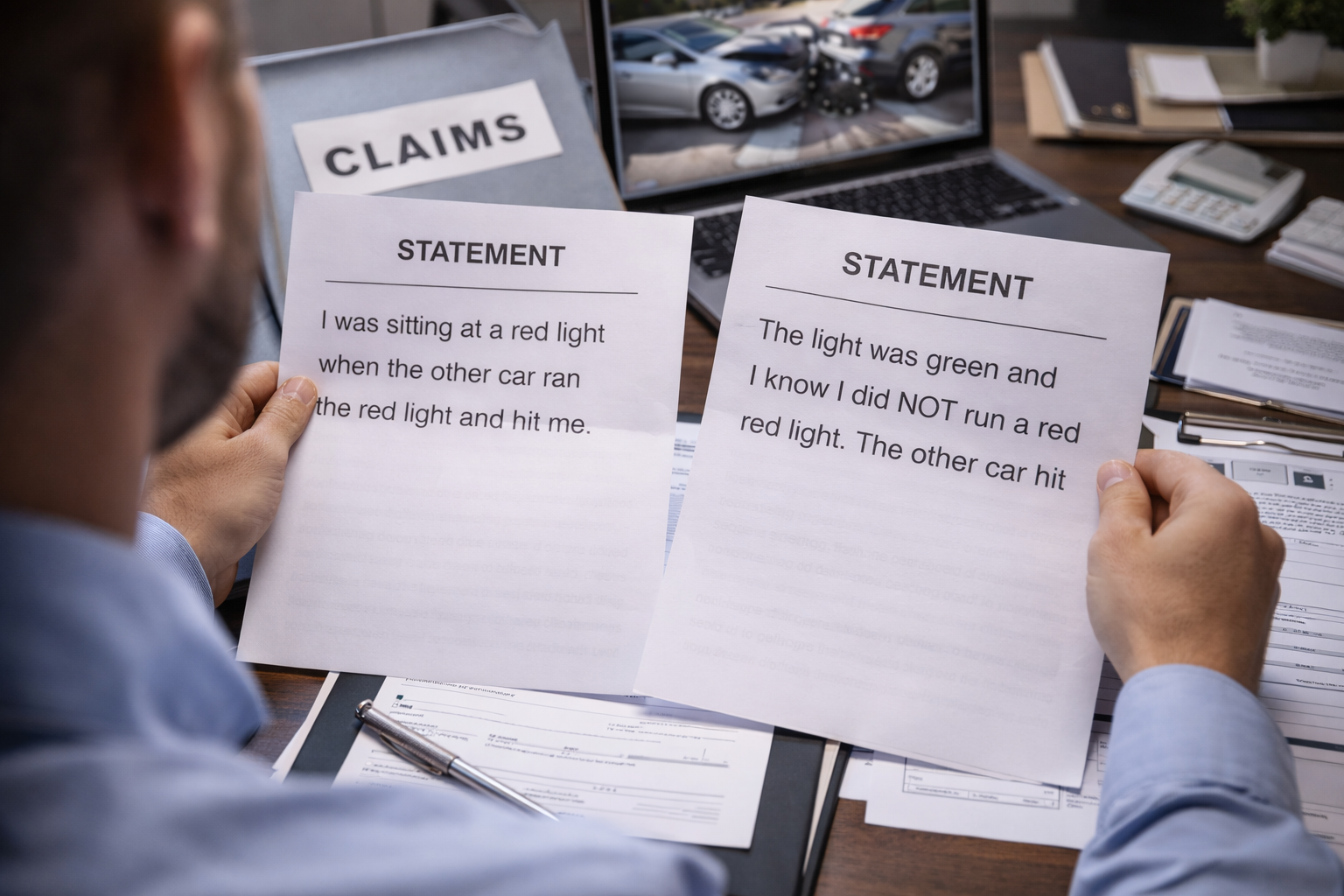

Mistake #3: Assuming Fault at the Scene

It’s natural for people to want to apologize after an accident.

But statements made at the scene don’t determine liability.

Drivers sometimes say things like:

“This was my fault.”

“I didn’t see you.”

“I’m so sorry.”

Those comments are often emotional reactions rather than accurate legal conclusions.

Determining fault requires reviewing evidence and traffic laws—not quick assumptions made during a stressful moment.

Mistake #4: Providing Inconsistent Information

Another challenge in claims investigations is conflicting statements.

Drivers may tell one version of events at the scene and later provide a different account to insurance companies.

Sometimes this happens because memories change or details become clearer later. Other times, people feel pressure and adjust their story.

But inconsistencies can complicate investigations and make it harder to determine what actually happened.

Providing clear and honest information from the beginning helps prevent unnecessary confusion.

Mistake #5: Ignoring Insurance Communication

Once a claim is opened, insurance adjusters typically reach out to gather information and move the investigation forward.

Sometimes drivers avoid calls or delay responses because they feel overwhelmed or uncertain about what to say.

But lack of communication can slow down the entire process.

Responding to requests for information helps ensure the claim progresses efficiently and allows adjusters to complete their investigation.

Mistake #6: Expecting Immediate Answers

Insurance investigations take time.

Adjusters often need to:

Review statements from multiple drivers

Evaluate vehicle damage

Examine photos or video evidence

Contact witnesses

Review police reports

While some claims are resolved quickly, others require more investigation before liability decisions can be made.

Patience during this process helps ensure that conclusions are based on accurate information rather than rushed assumptions.

Mistake #7: Hiring the Wrong Attorney — or Not Giving Them the Full Story

In some accident cases, drivers decide to hire an attorney to help handle the claim. For serious injuries or complicated liability disputes, legal representation can be very valuable.

But there are a few things many people don’t realize about how the process changes once an attorney becomes involved.

Your Attorney Becomes Your Spokesperson

Once you hire an attorney, insurance companies will usually stop communicating with you directly.

From that point forward, all communication typically goes through your attorney’s office.

That means when an insurance adjuster needs information about the accident, the questions are sent to your attorney, not to you.

If your attorney doesn’t have the information needed to answer those questions, the investigation can slow down.

In other words, the information the insurance company receives is only as complete as the information your attorney has available.

Providing your attorney with accurate and detailed information helps ensure they can respond effectively during the claims process.

The Process Doesn’t Change — Only the Messenger

Another common misconception is that hiring an attorney completely changes how a claim is evaluated.

In reality, the process is largely the same whether someone has legal representation or not.

Insurance companies still review:

Evidence from the accident

Police reports

Vehicle damage

Medical records

Witness statements

Applicable traffic laws

The difference is simply who communicates that information.

Instead of speaking directly with the driver involved in the accident, the insurance company communicates with the attorney representing them.

Choosing an Attorney Based Only on Promises

After an accident, some drivers are drawn to attorneys who advertise large settlements or quick payouts.

The reality is that no attorney can guarantee a specific settlement amount. Every claim depends on factors such as:

The severity of injuries

Medical treatment and documentation

Available insurance coverage

Liability evidence

State laws

Sometimes attorneys who make bold promises early in the process simply don’t have enough information yet to know what the case is truly worth.

Choosing representation based on experience, communication, and reputation is usually more important than choosing someone who promises the biggest number.

Always Give Your Attorney the Full Picture

Another issue that occasionally arises is when clients unintentionally leave out important details.

Attorneys can only represent their clients effectively when they have all the facts.

For example, a driver might forget to mention:

A prior accident

A pre-existing injury

Something they said at the scene

A dash camera recording

Witnesses who were present

Attorneys rely on accurate information to represent their clients effectively. If important facts emerge later during the investigation, it can weaken the case or create complications.

Providing complete and honest information from the beginning allows attorneys to prepare the strongest possible strategy.

Sometimes Attorneys and Insurance Companies Are Solving the Same Puzzle

It may surprise some drivers to learn that, in many cases, attorneys and insurance companies are actually working toward the same goal:

Understanding what happened and resolving the claim based on the available evidence.

While negotiations can sometimes become adversarial, both sides are ultimately evaluating the same things:

Liability evidence

Medical documentation

Insurance policy limits

Applicable laws

The strongest cases are usually the ones supported by clear documentation and consistent evidence, regardless of whether an attorney is involved.

The truth is, many claims settle through cooperation between attorneys and insurance companies once both sides have reviewed the available evidence.

Mistake #8: Expecting a Massive Settlement for Minor Injuries

After an accident, many drivers assume that any injury automatically leads to a large settlement.

This belief often comes from advertising, social media, or stories about major injury lawsuits.

The reality is much simpler.

Most auto accident claims involve minor injuries and relatively small settlements.

Insurance companies evaluate injury claims based on several factors, including:

Medical treatment received

Medical bills

Length of recovery

Documentation from doctors

Impact on daily activities

Evidence connecting the injury to the accident

If someone experiences minor soreness, visits a doctor once, and recovers quickly, the claim value will usually reflect that level of injury.

That doesn’t mean the injury wasn’t real. It simply means the compensation is tied to the documented impact of the injury.

Why Attorney Fees Can Change the Final Amount

Another factor people sometimes overlook is attorney fees.

Most personal injury attorneys work on a contingency fee, meaning they receive a percentage of the settlement.

This percentage is often around 30–40%, though it can vary.

For example:

If a claim settles for $5,000, and attorney fees are 33%, the attorney may receive approximately $1,650 before additional costs.

The remaining amount is then used to address medical bills or other expenses.

This doesn’t mean hiring an attorney is a mistake. In serious injury cases, legal representation can be extremely helpful.

But it’s important for drivers to understand how settlements are structured and how fees affect the final payout. The goal of a claim isn’t to “win.” The goal is to fairly resolve the damages based on the available evidence.

A Real-World Example from My Claims

Real Claim Example #1: Negotiation Didn’t Change the Final Outcome

To understand how settlement math sometimes works, consider a real example from a bodily injury claim I worked on a few weeks ago.

I received the injury claim on my desk and initially offered $2,500 to resolve the injury claim on day 8 based on the medical documentation and circumstances of the accident.

The claimant didn’t feel the offer was high enough and decided to hire an attorney. The attorney demanded $5,000 during negotiations.

After some back and forth, the claim eventually settled for $4,000.

At first glance, that sounds like a victory. The settlement increased by $1,500.

But once attorney fees were applied, the math changed.

The client walked away with $2,500 in pocket anyway… on day 53.

In other words, after the negotiation and legal fees, the client ended up with the same amount they could have received from the original offer 45 days earlier.

This doesn’t mean hiring an attorney is always a bad decision. In many serious injury cases, attorneys are extremely valuable and can help secure fair compensation.

But it does highlight an important reality:

Settlement amounts, attorney fees, medical bills, and negotiations all affect what someone ultimately receives.

Understanding how those pieces interact helps people make informed decisions during the claims process.

Real Claim Example #2: An Attorney Uncovered Important Information

In another claim, the initial evaluation resulted in a settlement offer of $3,000.

The claimant then hired an attorney.

During the attorney’s investigation, it was discovered that the claimant had experienced a separate workplace injury just three days before the accident that significantly worsened their condition. I had asked about prior injuries but the claimant decided I didn’t need to know and told me no, there were no aggravated injuries.

That information changed the overall evaluation of the claim.

The attorney ultimately negotiated a settlement of $10,000.

In this case, legal representation helped uncover additional context that increased the value of the claim.

Real Claim Example #3: High Demands Don’t Always Mean Higher Settlements

In another case, an attorney demanded $100,000 for a bodily injury claim involving a policy with $25,000 limits.

The claim was disputed and negotiated for more than six months.

Eventually, the claim settled for $15,000.

While negotiations can sometimes increase settlement values, the final outcome still depends heavily on the strength of the evidence and the limitations of the available insurance coverage.

The Most Important Factor: Documentation

The strength of any injury claim ultimately comes down to documentation.

Claims supported by detailed medical records, consistent treatment, and clear evidence tend to be easier to evaluate.

Claims with little or no documentation are much harder to support.

This is why seeking appropriate medical care and keeping records of treatment can be important after an accident.

Reality From the Claims Desk

Most accident claims are resolved for hundreds or a few thousand dollars—not the massive payouts often seen in advertisements.

Every claim is unique, but the final outcome almost always depends on evidence and documentation rather than expectations.

After a car accident, the insurance process can feel unfamiliar and sometimes frustrating.

But most claims move more smoothly when drivers focus on a few key principles:

Document the scene carefully.

Report the accident promptly.

Provide clear and consistent information.

Stay responsive during the investigation.

These simple steps help ensure that the claim process remains focused on what matters most:

Understanding what happened and resolving the situation fairly.